![]()

|

|

| INDEX

| Evolution | Sales

| by

country | back

| next |

|

Evolution

(by volume) |

|||||||||||||||||||||||||||||||||||||||||||||||

|

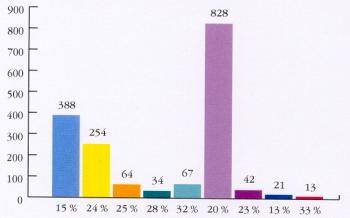

A sector that is increasingly geared to foreign markets : exports are up by 2 points between 1997 and 1998 and by 12 points in eight years. |

||||||||||||||||||||||||||||||||||||||||||||||

- top -

|

European

Exports |

Whilst most trade remains concentrated whitin the European countries, sales outside the European Union represent 20 % of the total exports in 1998, showing a decrease due to the crisis in Asia | ||||||||||||||||||||||

|

- top -

|

European

exports

|

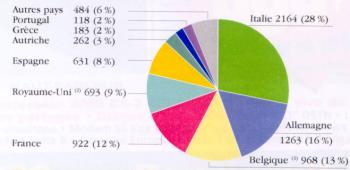

Italy maintains its leading position in European yarn exports by value, follwed by Germany, Belgium and France. |

||||

| (1)

the whole of Benelux for continuous-filament yarns (2) including Ireland for Linen. |

|||||

The European spinning Industry - Economic Dossier - -A study produced by the Institut Français de la Mode on behalf of EXPOFIL

© TEXMONDO - 2000 - Published with the kind agreement of Expofil